The Solar Photovoltaics Supply Chain Review explores the global solar photovoltaics (PV) supply chain and opportunities for developing U.S. manufacturing capacity. The assessment concludes that, with significant financial support and incentives from the U.S. government as well as strategic actions focused on workforce, manufacturing, human rights, and trade, America could reestablish a robust domestic solar manufacturing supply chain and become a competitive leader in a global solar industry. This could lead to tremendous benefits for the climate as well as for U.S. workers, employers, and the economy.

To achieve the Biden Administration’s goal of 100% clean electricity by 2035, solar energy would need to grow from 4% of electricity supply today to 40%, dramatically increasing demand for solar modules and components. This rapid expansion of solar energy has the potential to yield broad benefits in the form of economic activity, improved public health, and workforce development.

Produced by the U.S. Department of Energy (DOE) Solar Energy Technologies Office (SETO) with support from the National Renewable Energy Laboratory (NREL) and released on February 24, 2022, this is one of a series of energy sector industrial reports directed through President Biden’s Executive Order 14017 “America’s Supply Chains.” The Executive Order will help the U.S. federal government to build more secure and diverse U.S. energy supply chains – facilitating greater domestic production, an acceleration in clean energy, a range of supply, built-in redundancies, adequate stockpiles, safe and secure digital networks, and a world-class American manufacturing base and workforce.

Key Findings

- Developing U.S. PV manufacturing could mitigate global supply chain challenges and lead to tremendous benefits for the climate as well as for U.S. workers, employers, and the economy.

- The solar supply chain is global and reliant on products from China or companies with close ties to China, a country with documented human rights violations and an unpredictable trade relationship with the United States.

- Significant growth in U.S. manufacturing across the supply chain is possible with incentives that offset the higher cost of manufacturing in the United States.

- Existing polysilicon production facilities are currently idle or supplying polysilicon to other industries. Expansion in the ingot and wafer sectors outside of China would create demand for existing U.S. polysilicon producers to run at high capacity.

- The United States can expand production of thin-film modules, which do not rely on obtaining materials from Chinese companies. The thin film supply chain is concentrated in Ohio.

Frequently Asked Questions

The supply chain for solar PV has two branches in the United States: crystalline silicon (c-Si) PV, which made up 84% of the U.S. market in 2020, and cadmium telluride (CdTe) thin film PV, which made up the remaining 16%.

The supply chain for c-Si PV starts with the refining of high-purity polysilicon. Polysilicon is melted to grow monocrystalline silicon ingots, which are sliced into thin silicon wafers. Silicon wafers are processed to make solar cells, which are connected, sandwiched between glass and plastic sheets, and framed with aluminum to make PV modules. Then, they are mounted on racking or tracking structures and connected to the grid using a power electronics device called an inverter.

The supply chain for CdTe PV starts with refining cadmium and tellurium to high-purity powders, which are then deposited directly onto a glass sheet. Another piece of glass and plastic sealant are applied to finish the module, which then can be mounted and connected to the grid in an identical fashion to c-Si modules.

The primary inputs to the global solar supply chain include: metallurgical-grade silicon (MGS), glass, resins to make plastic sheets (encapsulant and backsheet), and aluminum. MGS is produced from high-grade quartz. Quartz is a compound of silicon and oxygen, the two most abundant elements in the earth’s crust.

As of 2021, China possessed 72% of the world’s polysilicon manufacturing capacity, 98% of ingots, 97% of wafers, 81% of cells, and 77% of modules. Seventy-five percent of the silicon solar cells incorporated into modules installed in the United States are produced by Chinese subsidiaries operating in three Southeast Asian countries: Vietnam, Malaysia, and Thailand. The two largest tracker vendors were the U.S. firms Nextracker and Array Technologies, collectively representing 70% of 2020 U.S. tracker shipments, and 46% of 2020 global tracker shipments. Globally, in 2020, 66% of PV inverters were manufactured by companies headquartered in China. However, the U.S. market relied more on inverters from companies headquartered in Europe and Japan.

While the country has considerable polysilicon production capacity, as of 2021, it was not being used for solar applications. There was also no active ingot, wafer, or silicon cell manufacturing capacity. Using imported cells, about 2 GW of c-Si modules were made domestically in 2020. An additional 25 GW of c-Si modules were imported, 75% of them from Chinese companies operating in Southeast Asia.

The United States does have production capacity for CdTe technology, which does not rely on obtaining materials from Chinese companies. The 16% of U.S. solar PV installations that used CdTe were supplied by a single U.S. company, and one-third of their modules are made in the United States.

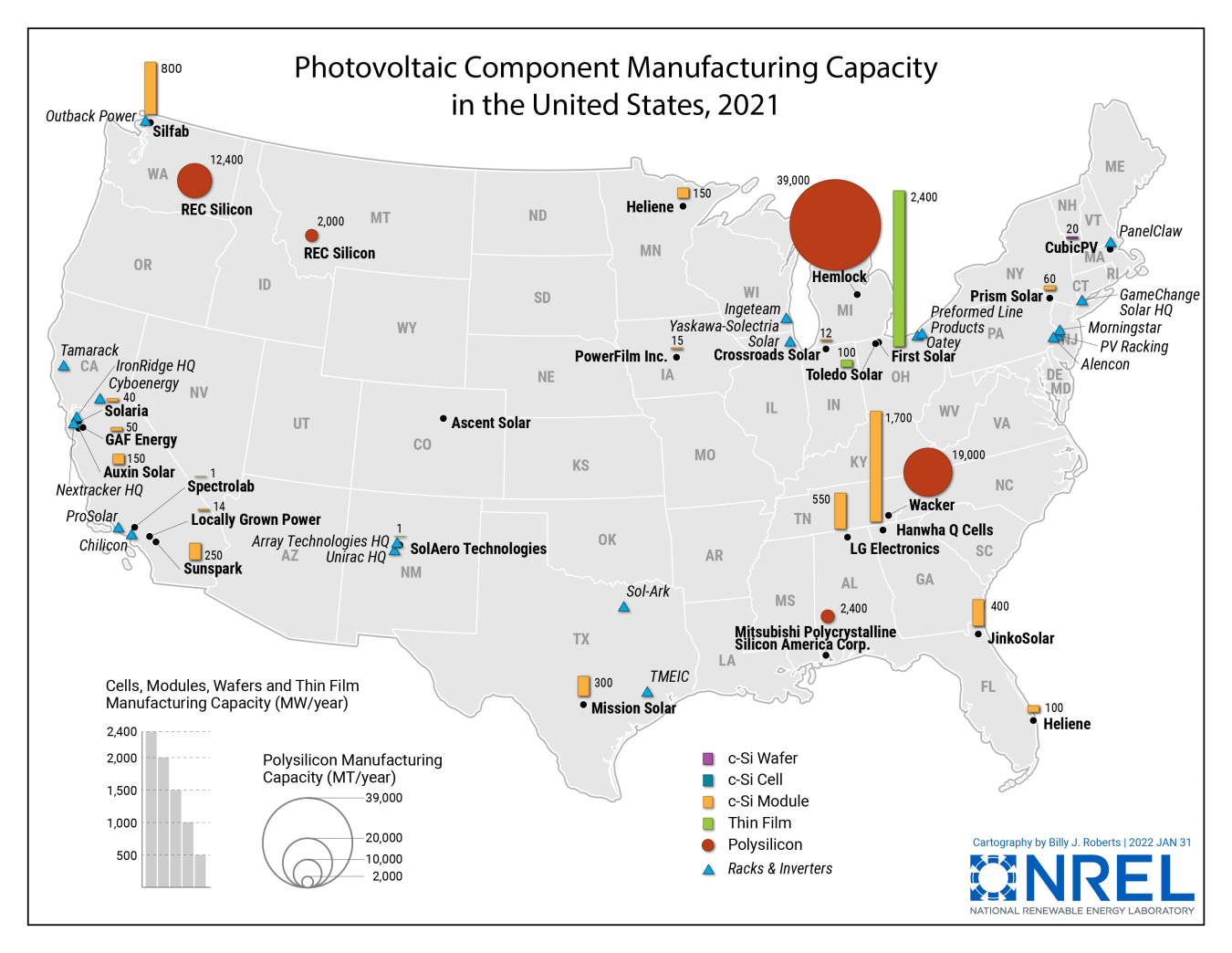

The U.S. Photovoltaic Component Manufacturing Capacity map includes any active manufacturing site in the U.S. and their nameplate capacity, or the full amount of potential output at an existing facility, as of January 31, 2022. This does not imply that these facilities produced the amount listed. The data comes from public sources and direct communication with producers. This data is subject to change and is for general informational purposes only. SETO/NREL does not guarantee that the data is complete or free of error.

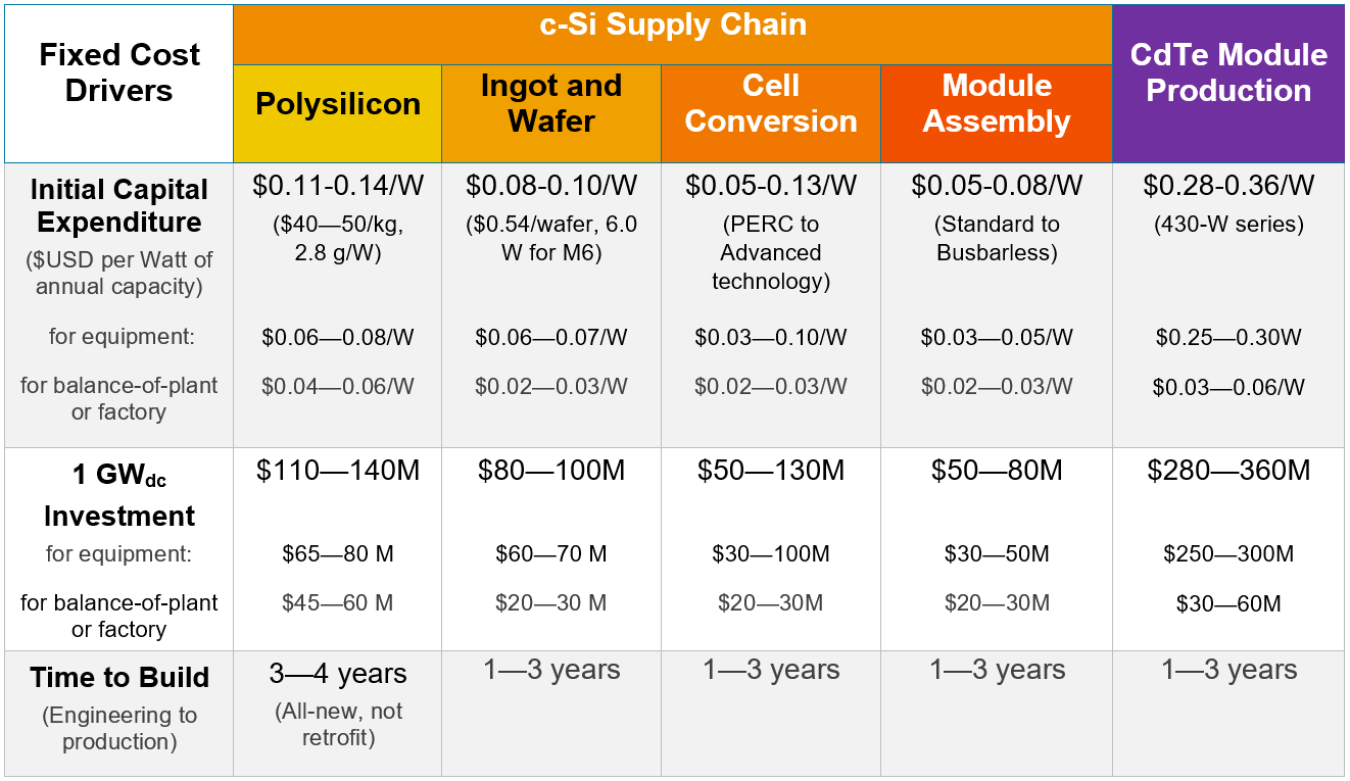

The time to build new facilities, the minimum scale of these facilities, and the capital expenditures vary by manufacturing step and supply chain component. Facilities for certain steps, such as module assembly, are less expensive and faster to scale than others, such as ingot and wafer production.

Fixed-cost drivers across the c-Si and CdTe supply chain. Source: NREL (Smith et al. 2021).

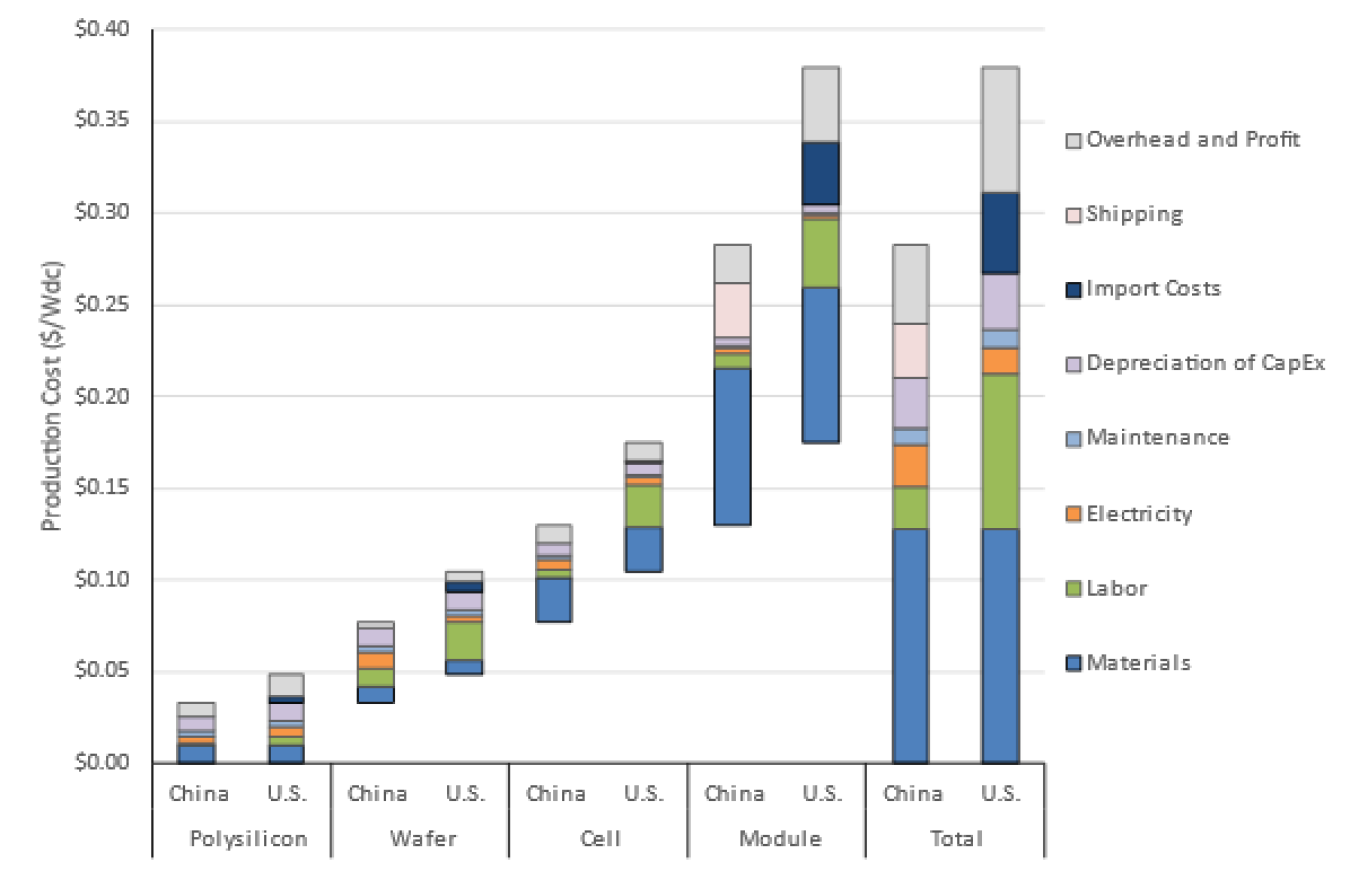

Manufacturing silicon modules in the United States in 2020 cost 30-40% more than in China due to China’s low labor costs, concentrated supply chain, and non-market practices. Labor is the primary driver of the cost differences, representing 22% of total U.S. manufacturing costs versus 8% in China. Import costs are also a factor, adding about 11% to U.S. manufacturing costs. This is due to gaps in the PV supply chain, which require the importing of components like aluminum frames, glass, and cells.

Production Costs for c-Si PV Manufacturing in the United States and China in 2020

The cost to produce a CdTe module in the United States in 2020 is approximately the same as that of Southeast Asia, when accounting for shipping. Source: NREL.

The cost to produce a CdTe module in the United States in 2020 is approximately the same as that of Southeast Asia, when accounting for shipping. Source: NREL.The United States does have production capacity for CdTe modules, which can be scaled-up to the limit that material availability allows, with little risk of being overtaken by low-cost foreign competition. However, no alternate PV technology, including CdTe, can displace c-Si quickly enough to achieve power sector decarbonization by 2035.

Current silicon wafer manufacturing strategies waste about one-third of the crystalline silicon material. Research into less wasteful methods is ongoing because the cost advantage is substantial and market acceptance is almost certain for any wafer that meets the specifications of cell producers.

The country that establishes the international standards for PV inverters will have a first-mover advantage, providing a window of opportunity to restore U.S. competitiveness in PV inverter design and manufacturing.

The United States would benefit from being the first to commercialize perovskite PV technology. However, it would be unprecedented for such a new PV technology to have a significant market impact in the timeframe required for decarbonization by 2035, and the United States faces intense competition from China, Europe, and Japan in the commercialization of perovskites.

Learn more about the solar manufacturing research funded by SETO.

At the federal level, the United States has implemented many measures to encourage domestic PV manufacturing including past tax credits, federal loans, and federal procurement to increase domestic solar demand. At state and municipal levels, policies intended to support domestic PV manufacturing have included grants, tax exemptions, land provision, and consumer incentives for purchasing domestic PV products.

The United States has also attempted to support domestic PV manufacturing through the implementation of several tariffs over the past 10 years. Antidumping and Countervailing Duties (AD/CVD) were placed on Chinese (and to a lesser extent Taiwanese) PV modules and cells in 2012 and 2014, as well as imported MGS in 2018 and 2021. In 2018, safeguard (Section 201) tariffs were also instituted on all imported PV cells and modules, exempting the first 2.5 GWdc of PV cells to support domestic module assembly, plus additional tariffs (Section 301 and Section 232 tariffs) on inputs to the solar supply chain.

The solar supply chain has also been impacted by U.S. policies addressing concerns regarding forced labor. A Withhold Release Order (WRO) was issued in June 2021 against shipments containing material produced from silica-based products made by the Chinese company Hoshine Silicon Industry Co. Ltd and its subsidiaries following reports linking it to forced labor in Xinjiang. Signed into law in December 2021, the Uyghur Forced Labor Prevention Act (UFLPA) presumptively prohibits all products originating in Xinjiang, including polysilicon, from being imported into the United States unless an importer can prove via clear and convincing evidence that an entity’s goods are not produced using forced labor.

The concentration of the c-Si supply chain in companies with close ties to China, a country with documented human rights violations and an unpredictable trade relationship with the United States, poses a significant risk of disruption to the c-Si supply chain. Additionally, developing U.S. PV manufacturing would benefit U.S. workers, employers, and the economy.

Additional Resources

- Download the summarized Solar Photovoltaics Supply Chain Review fact sheet.

- Download the full Solar Photovoltaics Supply Chain Review.

- Read the DOE announcement.

- Browse the other DOE energy sector industrial supply chain reports.

- View SETO’s goals.

- Explore SETO’s research in photovoltaics and manufacturing and competitiveness.

- Learn about solar photovoltaic manufacturing basics.