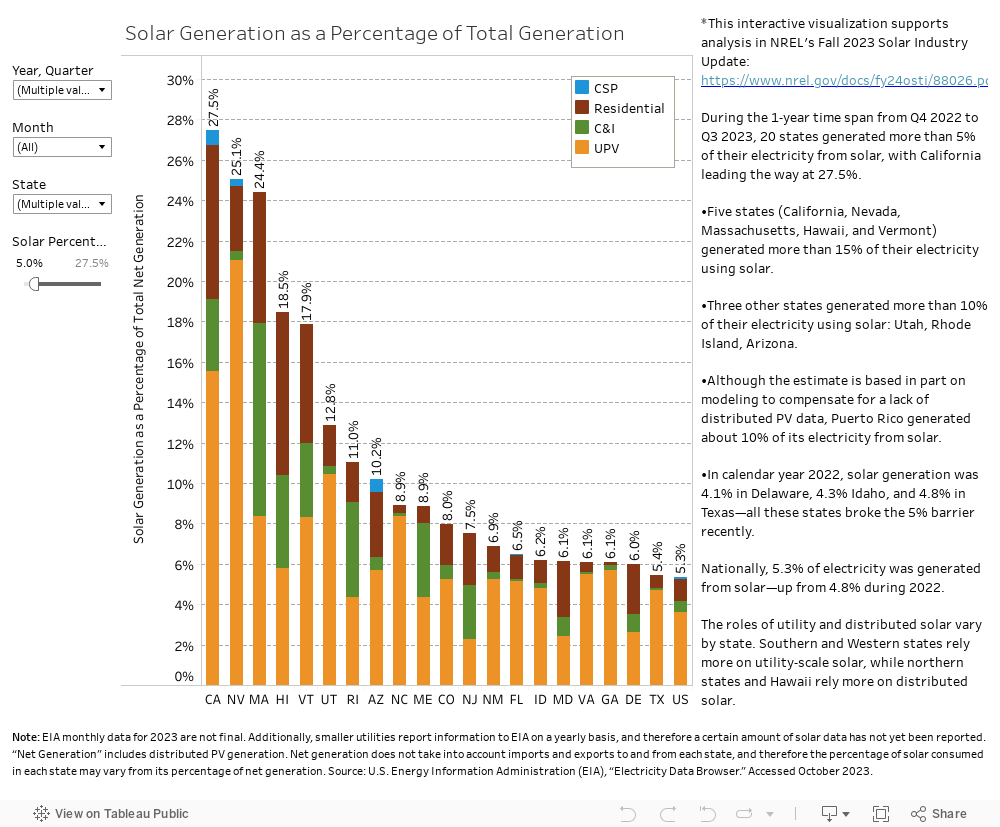

Each quarter, the National Renewable Energy Laboratory conducts the Quarterly Solar Industry Update, a presentation of technical trends within the solar industry. Each presentation focuses on global and U.S. supply and demand, module and system price, investment trends and business models, and updates on U.S. government programs supporting the solar industry.

Download the latest report: Fall 2024 Quarterly Solar Industry Update

Key updates from the Fall 2024 Quarterly Solar Industry Update presentation, released October 30, 2024:

Global Solar Deployment

- The International Renewable Energy Agency (IRENA) reports that, between 2010 and 2023, the global weighted average levelized cost of energy of concentrating solar power (CSP) fell from $0.39/kilowatt-hours (kWh) to under $0.12/kWh—a decline of 70%.

- IRENA reports significant cost declines for all cost drivers within a CSP system, leading total capital expenditure (CAPEX) for parabolic trough and power tower CSP plants to decline 58% and 68%, respectively, from 2010/2011 to 2023.

- Several CSP projects are underway to provide 100-hour+ energy storage.

U.S. PV Deployment

- The International Energy Agency projects significant growth for photovoltaics (PV) in 2024 over the record-breaking year in 2023. Over the next two years, virtually all new electric generation capacity will be PV, batteries, and wind.

- The United States installed approximately 14.1 gigawatt (GW)-hours (4.3 GW alternating current [GWac]) of energy storage onto the electric grid in the first quarter (Q1)/second quarter (Q2) of 2024—its largest first half on record.

- Though thin-film PV represented around 3% of global PV deployed from 2015 through 2023, it accounted for more than 17% of U.S. PV deployments during this period (24% of utility-scale deployments).

- In 2023, approximately 45% of battery capacity and 26% of utility-scale PV capacity were hybrid PV/battery energy storage system projects—relatively consistent with previous years.

- The third-party ownership share of U.S. residential PV systems increased sharply in 2024, aided by high interest rates and additional incentives from the Inflation Reduction Act (IRA).

PV System and Component Pricing

- Most data suggest decreases in CAPEX in the first half of 2024, but energy pricing across market segments varied because of other factors.

- In the third quarter (Q3) of 2024, module prices rose 1% but stayed near record lows, around $0.10/ Watt direct current (Wdc), as substantial module overcapacity continues to depress prices.

- Global polysilicon spot prices rose 3% from early August ($5.66/kilograms [kg]) to early October ($5.86/kg); however, prices are still below production costs for most manufacturers.

- In Q2 2024, the average U.S. module price ($0.31/Wdc) was down 6% quarter-over-quarter and down 16% year-over-year (y/y), and at a 190% premium over the global spot price.

- In Q3 2024, the average imported PV cell price was $0.12/Wdc.

Global Manufacturing

- According to Infolink, the top 10 module manufacturers were responsible for 226 GW of shipments (+40% y/y) in the first half of 2024.

- In the first half of 2024, the United States produced 4.2 GW of PV modules—an increase of 75%, y/y—roughly evenly split between thin-film and crystalline silicon (c-Si) module technology.

- Since the IRA’s passage, more than 95 GW of manufacturing capacity have been added across the solar supply chain (from facilities announced pre- and post-IRA), including nearly 42 GW of new module capacity.

- U.S. c-Si manufacturers added significant capacity in the first half of 2024.

- Analysts estimated that U.S. c-Si cell production and capacity should begin to slowly ramp up in the second half of 2024.

- On October 22, the Internal Revenue Service clarified that domestic solar ingot and wafer producers can receive the 25% 48D investment tax credit.

U.S. PV Imports

- According to U.S. Census data, in Q3 2024, U.S. module imports grew again to nearly 15.4 GWdc or 48.5 GWdc for the first 9 months of 2024.

- On October 1, 2024, the U.S. Department of Commerce issued a preliminary decision to impose countervailing duties on c-Si panels and cells produced in Vietnam, Malaysia, Thailand, and Cambodia. Tariffs ranged from 0% to 300%; a preliminary decision on antidumping duties is expected later.

- According to a U.S. Customs and Border Protection Commodity Status Reports, since the President raised the annual tariff rate quota for cells to 12.5 GW in August, imports have continued to accelerate. As of Oct. 28, 2024, more than 9.4 GW (75% of the tariff-rate quota) of cells have been imported.

Presentations

Presentations are available for download in PDF format below.

2024

- Fall 2024 Presentation – Released December 30, 2024

- Summer 2024 Presentation – Released August 20, 2024

- Spring 2024 Presentation – Released May 14, 2024

- Winter 2024 Presentation – Released January 25, 2024

2023

- Fall 2023 Presentation – Released October 26, 2023

- Summer 2023 Presentation – Released August 3, 2023

- Spring 2023 Presentation – Released April 27, 2023

- Winter 2023 Presentation – Released January 26, 2023

2022

- Fall 2022 Presentation – Released October 27, 2022

- Summer 2022 Presentation – Released July 12, 2022

- Spring 2022 Presentation – Released April 26, 2022

2021

- Winter 2021-2022 Presentation – Released January 11, 2022

- Fall 2021 Presentation – Released October 20, 2021

- H1 2021 Presentation – Released June 22, 2021

2020

- Q3/Q4 2020 Presentation – Released April 6, 2021

- Q2/Q3 2020 Presentation – Released December 8, 2020

- Q1/Q2 2020 Presentation – Released September 1, 2020

2019

- Q4 2019/Q1 2020 Presentation – Released June 19, 2020

- Q3/Q4 2019 Presentation – Released February 18, 2020

- Q2/Q3 2019 Presentation – Released November 12, 2019

- Q1/Q2 2019 Presentation – Released August 6, 2019

2018

- Q4 2018/Q1 2019 Presentation – Released June 14, 2019

- Q3/Q4 Presentation – Released February 7, 2019

- Q2/Q3 Presentation – Released December 3, 2018

- Q1/Q2 Presentation – Released August 17, 2018

2017

- Q4 2017/Q1 2018 Presentation - Released May 16, 2018

- Q3/Q4 Presentation – Released February 6, 2018

- Q2/Q3 Presentation – Released November 13, 2017

- Q1/Q2 Presentation – Released August 28, 2017

2016

- Q4 2016/Q1 2017 Presentation – Released May 18, 2017

- Q3/Q4 Presentation – Released January 17, 2017

- Q2/Q3 Presentation – Released October 17, 2016

Subscribe to the Solar Energy Technologies Office Newsletter