Bottom-up assessment of policies and market conditions that may impact future utility electricity efficiency programs

Office of Critical Minerals and Energy Innovation

December 3, 2018

Electricity efficiency programs funded by utility customers cost-effectively offset a portion of growth in U.S. power needs. That, in turn, affects the need for investment in new electricity infrastructure, across generation, transmission and distribution systems. A new study by Berkeley Lab provides a bottom-up assessment of the potential impact of existing and likely state policies and market conditions to promote or constrain future spending and savings for electricity efficiency programs in all U.S. states.

The new study includes three scenarios—low, medium and high cases—for 2030, with projections of spending and savings for interim years. The scenarios represent different pathways for the evolution of electricity efficiency programs funded by utility customers given the current policy environment and uncertainties in the broader economic and state policy environment in each state.

Among the key findings of the study:

- Spending on electricity efficiency programs is expected to rise to $8.6 billion in 2030 in the medium case, an increase of more than 45 percent compared to 2016. In the high case, annual spending increases by 90 percent compared to 2016 levels, reaching $11.1 billion in 2030. Spending in the low case remains fairly flat, increasing to only $6.8 billion in 2030.

- Regional shares of national spending are expected to shift over time. In 2016, states in the West and Northeast accounted for 64 percent of national spending on electricity efficiency programs, while states in the South and Midwest accounted for 36 percent. In 2030, these values represent the estimated shares of national spending in the low scenario. In the high scenario, the relative share of spending in 2030 for states in the West and Northeast decreases to 55 percent of the national total, while states in the South and Midwest account for 45 percent.

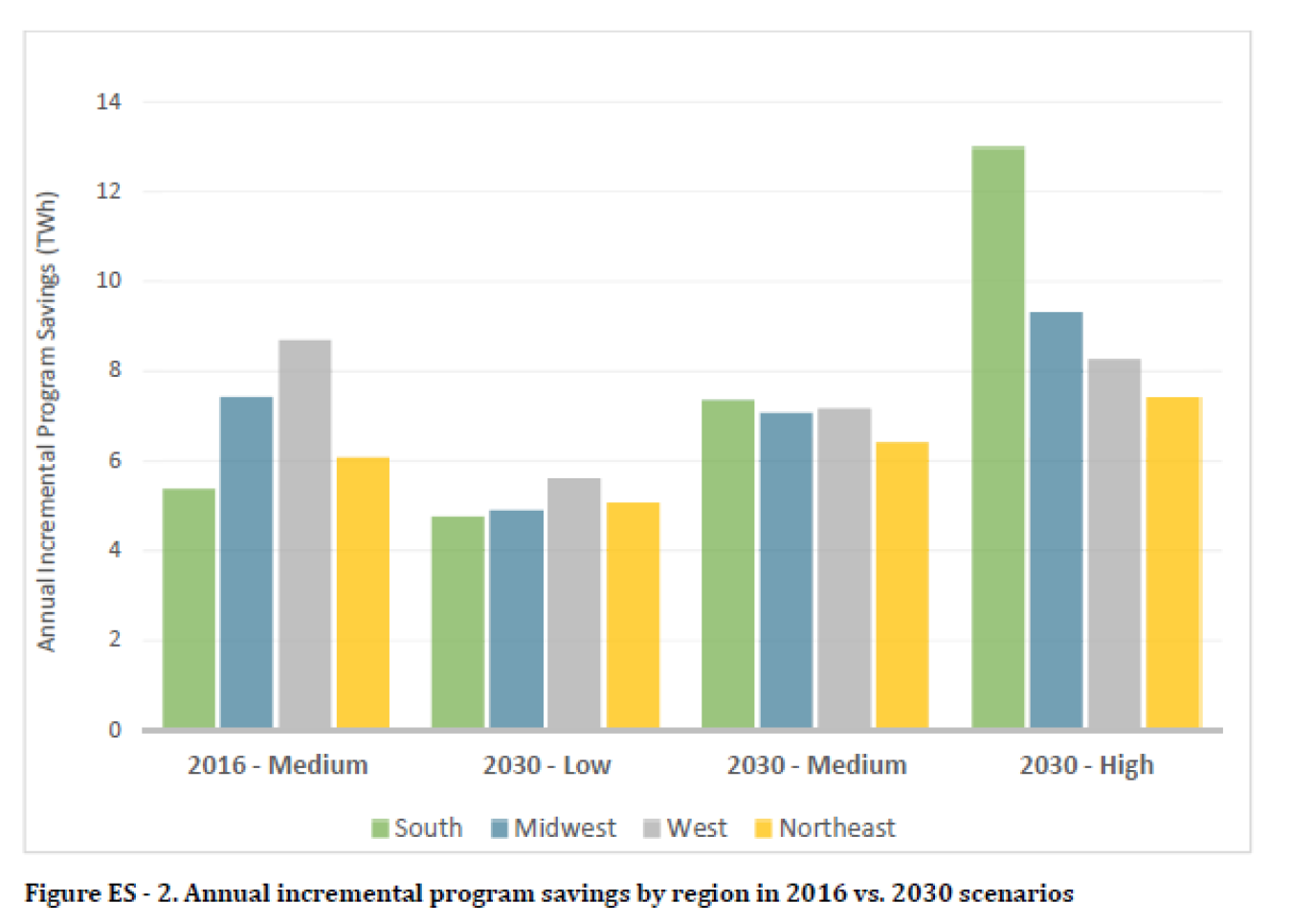

- Efficiency programs will continue to impact load growth at least through 2030. In the medium case, incremental annual electricity savings are expected to increase very modestly to 28 TWh in 2030. In the high case, annual savings increase to 38 TWh by 2030 (equal to about 1 percent of retail sales)—38 percent higher than savings achieved in 2016. Also in the high scenario, projected savings in the South are significantly greater compared to other regions. However, savings as a percent of retail sales in this 2030 scenario remain higher in other regions. In the low scenario, first-year savings are 27 percent lower compared to 2016.