WPTO published the U.S. Hydropower Market Report, which compiled data from public and commercial sources as well as DOE R&D projects.

Hydropower and Hydrokinetic Office

January 13, 2021In January 2021, WPTO will publish the third complete edition of the “U.S. Hydropower Market Report.” Previous surveys and feedback from readers shows the information about U.S. hydropower and industry trends is useful to a broad range of stakeholders and decision makers. Combining data from public and commercial sources, as well as DOE R&D projects, the seminal report provides the most comprehensive picture of developments in U.S. hydropower and PSH alongside national and global industry trends and future projections.

The publication is the third complete edition of the “U.S. Hydropower Market Report,” preceded by the 2014 and 2017 editions. This edition picks up where the 2017 report left off, covering the updated 2017–2019 data and contextualizing this information with high-level trends spanning the past 10–20 years. The publication was evaluated by 34 external reviewers from 24 organizations, ranging from turbine manufacturers and owners and operators of hydropower systems to federal agencies, consultancies, labs, and other associations and organizations.

Breaking trends down by region, plant size, owner type, and other attributes, the report also communicates updated information about the U.S. and global hydropower and PSH development pipeline and hydropower prices, and offers performance metrics for the period following the “2017 Hydropower Market Report.” The 2019 report discusses hydropower and PSH’s contributions to flexibility services and grid reliability, summarizing findings from DOE’s HydroWIRES Initiative.

Organized into seven chapters, the report includes a chapter looking back at changes across the U.S. hydropower and PSH fleet, as well as a chapter looking ahead to the future U.S. hydropower and PSH development pipeline. Chapters 3–7 examine U.S. hydropower in the global context, U.S. hydropower price trends, U.S. hydropower cost and performance metrics, trends in the U.S. hydropower supply chain, and policy and market drivers, respectively.

The report draws several important conclusions:

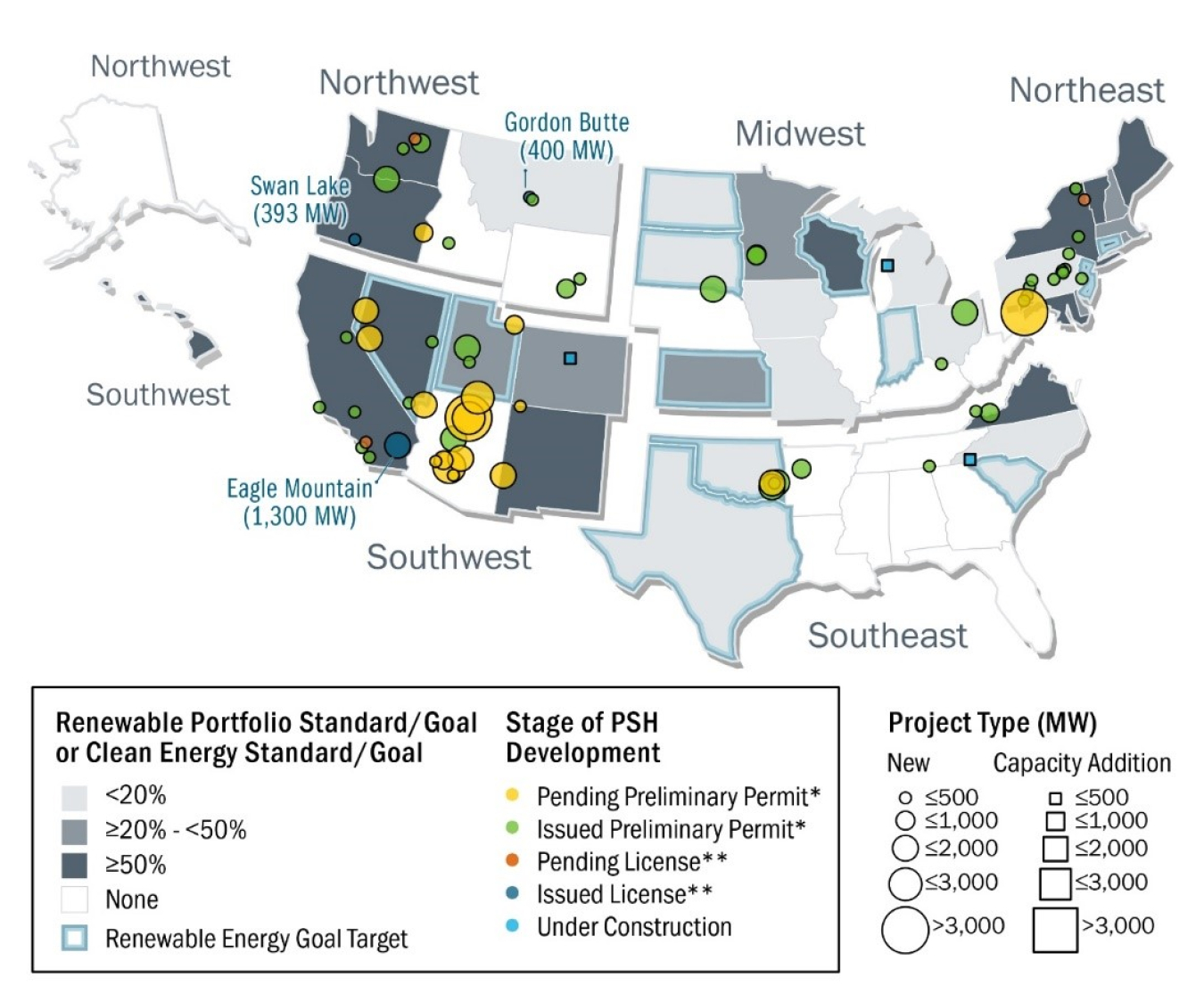

- Almost as much PSH capacity was added from 2010 to 2019 (1,400 MW)—mostly from upgrades to existing plants—as the combined installed capacity of all other forms of energy storage in the United States (1,675 MW).

- Interest in PSH in the United States continues to grow significantly, as evidenced by the doubling of the numbers of projects in the development pipeline over the past 5 years.

- Geographic interest in U.S. PSH has expanded as well, with new projects under exploration in Pennsylvania, Virginia, Wyoming, Oklahoma, Ohio, and New York.

- Internationally, there has been a significant and growing interest in PSH. At the end of 2019, 50 PSH projects under construction equated to 53 GW of capacity globally, with an additional 226 GW of PSH in development, essentially doubling the global fleet.

- Hydropower provides a plethora of ancillary services, punching well above its weight when compared to percent of installed capacity in nearly every region and by every metric analyzed, including black start, 1-hour ramps, frequency regulation, and reserves.

- At the end of 2019, a total of 128 projects constituting 669 MW of hydropower had been issued a FERC license, though construction had not yet been initiated; more than half of the projects had been in this state of limbo for 3 years or more.

- FERC relicensing activity is expected to more than double in the coming decade, with an estimated 4.7 GW of hydropower capacity and 9.1 GW of PSH capacity to be added.

For additional information, contact Brennan T Smith.

Hydropower Success Stories

-

In late 2019, PNNL’s new autonomous, mobile, water quality sensor platform was field-tested for the first time.

In late 2019, PNNL’s new autonomous, mobile, water quality sensor platform was field-tested for the first time. -

Three national laboratories are demonstrating the technical and economic benefit of integrating run-of-river plants with energy storage.

Three national laboratories are demonstrating the technical and economic benefit of integrating run-of-river plants with energy storage. -

In December 2020, WPTO announced 11 winners of the I AM Hydro Prize, a competition designed to help strengthen hydropower technologies.

In December 2020, WPTO announced 11 winners of the I AM Hydro Prize, a competition designed to help strengthen hydropower technologies. -

Pennsylvania State University has manufactured and validated a novel hydropower turbine-generator which can be deployed at various low-head sites.

Pennsylvania State University has manufactured and validated a novel hydropower turbine-generator which can be deployed at various low-head sites.