Learn how wind turbines are soaring to new heights.

Office of Critical Minerals and Energy Innovation

August 18, 2014

Turbines at the National Wind Technology Center in Boulder, Colorado. The 2013 Wind Technologies Market Report includes a new chapter that focuses on trends in wind turbine nameplate capacity, hub height, rotor diameter, class, and specific power. | Photo by Ben Chicoski

The Energy Department and Lawrence Berkeley National Laboratory today released the 2013 Wind Technologies Market Report, which examines the latest statistics and trends in the U.S. wind power market. For the first time in the report’s history, we have added a new chapter that details trends in wind turbine nameplate capacity, hub height, rotor diameter, class, and specific power.

This new Technology Trends chapter highlights several technology-based factors that point to strong future wind industry growth. Notably, the report finds that substantial turbine scaling—increasing the average turbine nameplate capacity, hub height, and rotor diameter—has occurred throughout the past decade. For example, the average nameplate capacity of newly installed turbines in 2013 was 1.87 megawatts (MW), up 162% since 1999. The average hub height of turbines installed in 2013 was 80 meters, up 45% from 1999. Also, 75% of installed turbines had a rotor diameter of 100 meters in length or more. Increased hub heights and larger rotors allow turbines to generate more renewable electricity, in part by taking advantage of the stronger, more consistent winds that are often found at higher altitudes.

This significant scaling has also enabled wind project developers to do two important things:

- Cost-effectively build projects at sites with lower wind speed while increasing projects’ overall capacity factors,

- Install turbines originally designed for lower wind speeds in higher wind speed sites, further boosting expected capacity factors.

These trends helps explain the increasing market share of turbines designed for lower wind speeds and their deployment in all regions of the country.

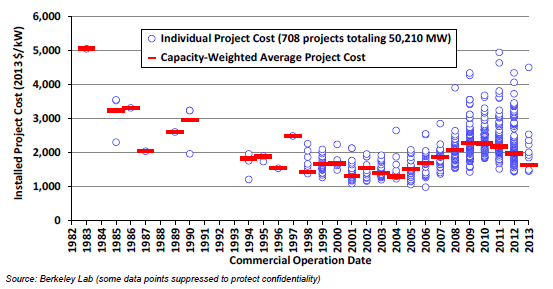

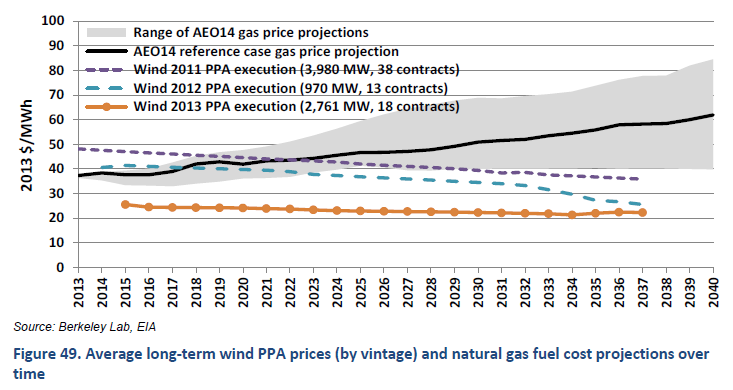

These technology developments, combined with lower wind turbine prices in the $900–$1,300 per kilowatt range, decreased total project costs and wind power prices in 2013. In fact, wind energy prices fell to the bottom of the range of nationwide wholesale power prices last year, and are projected to be in line with or lower than the fuel costs of gas-fired generation for two decades. (See charts below).

Installed Wind Power Project Costs Over Time

Average Long-Term Wind Power Purchase Agreement Price Projections

According to the report, state renewable portfolio standards policies, along with federal policy drivers such as the Production Tax Credit (PTC) and accelerated tax depreciation, will also help drive growth in the domestic wind power market for the next two years. Notably, while the PTC expired last year, projects that began construction by the end of 2013 were eligible for the tax credit; many of these projects will be commissioned over the next couple years.

These policy incentives, combined with turbine scaling, transmission line construction, and continued state leadership, are expected to stimulate robust growth of wind power capacity in the near term. According to the American Wind Energy Association, more than 14,000 megawatts of wind power capacity were under construction in the second quarter of 2014. All signs point to a strong wind industry and a growing renewable energy economy in the years to come. Read the 2013 Wind Technologies Market Report in full, and learn more about the Energy Department’s work to accelerate the deployment of wind power technologies through improved performance, lower costs, and reduced market barriers.